Coco Gauff Is Playing for Herself Now

18 MIN READ

At 20, the defending U.S. Open champion is moving into a new phase of her career

At 20, the defending U.S. Open champion is moving into a new phase of her career

A rare total solar eclipse will occur across Mexico, the U.S., and Canada on April 8, 2024, when the moon will pass between the Earth and the Sun, blocking the sun’s rays during the day time, causing a temporary period of darkness. TIME Editor-at-Large Jeffrey Kluger explains the best way to experience it.

Subscribe now to get unlimited access to TIME.com and more!

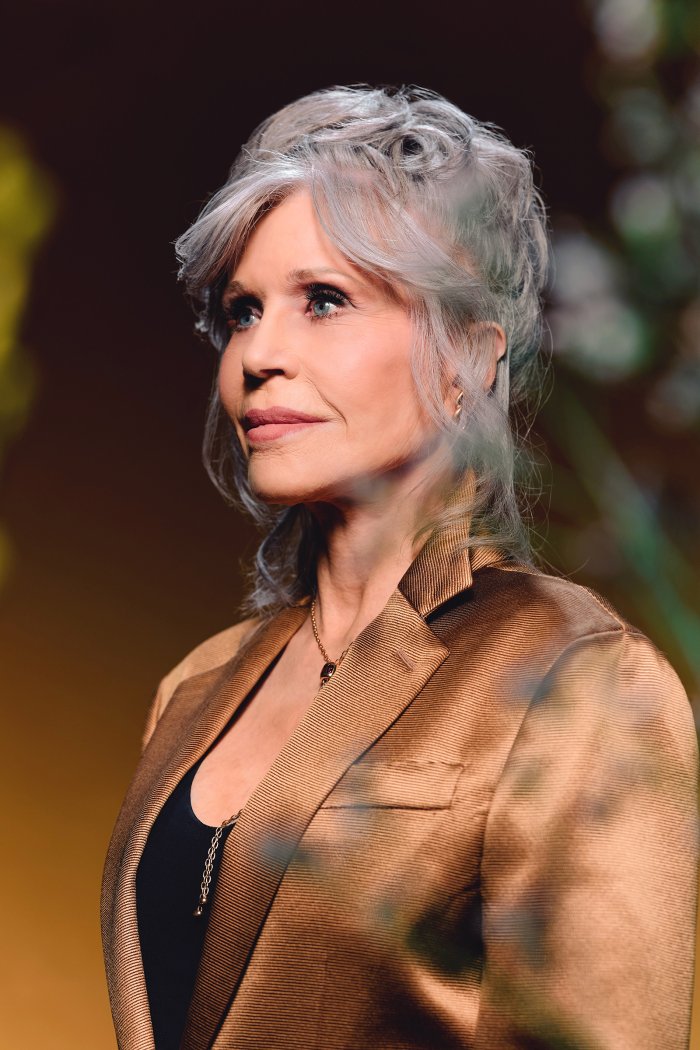

Biden "provides us a context in which we can fight,” Fonda said at the Time100 Summit.

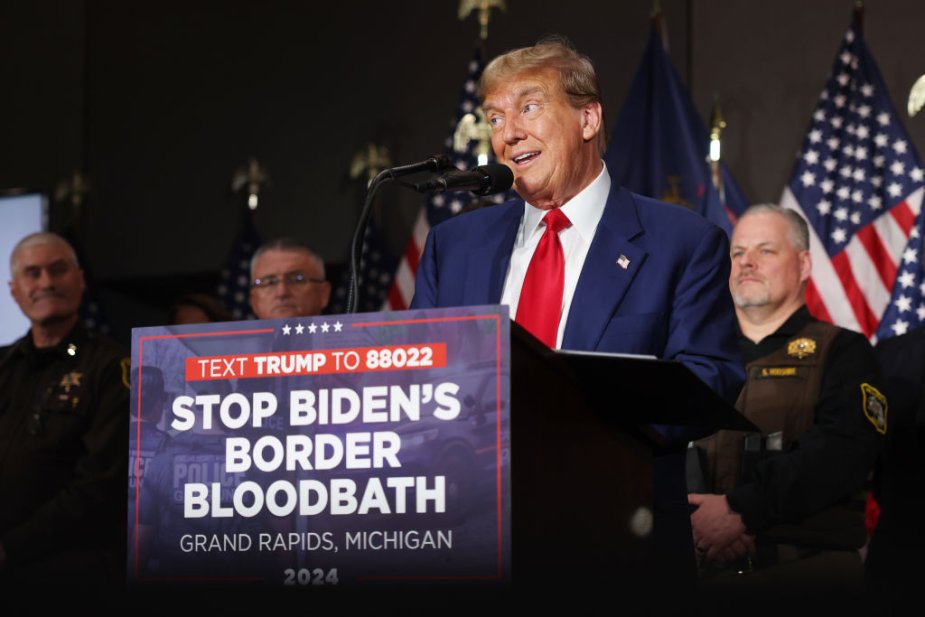

The judge overseeing the former president's criminal trial is familiar with his history, in and out of court.

Beyoncé fans are convinced she will be making a surprise appearance at the country music festival, Stagecoach. Here's what you need to know.

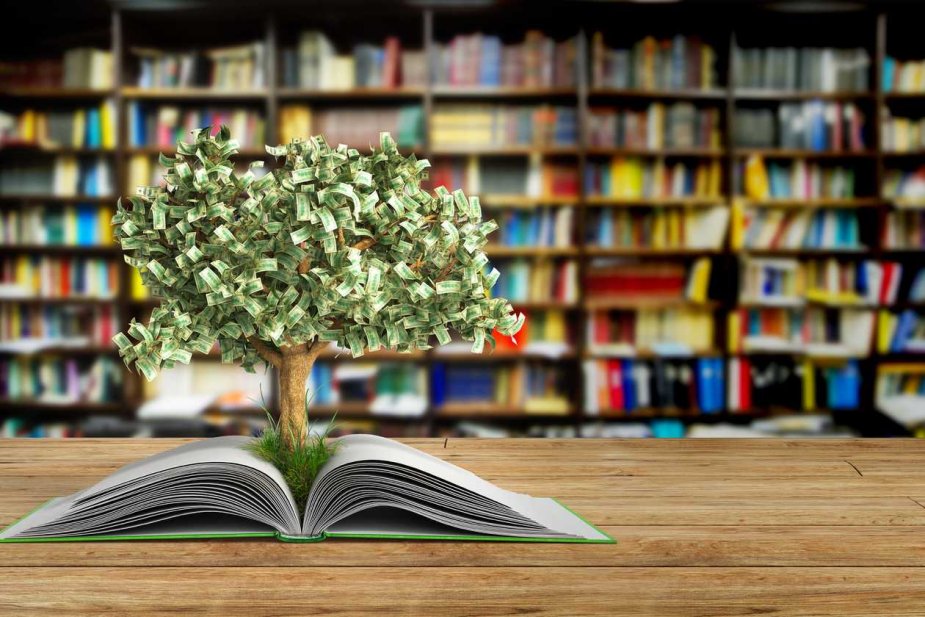

New research about incentives, collaboration, and connection.